Top 5 Digital Banking Myths: Community Banks Need to Abandon

Digital payments are already here, whether we are ready for it or not. With every passing day, there are FinTech companies continually pushing the digital payment envelope.

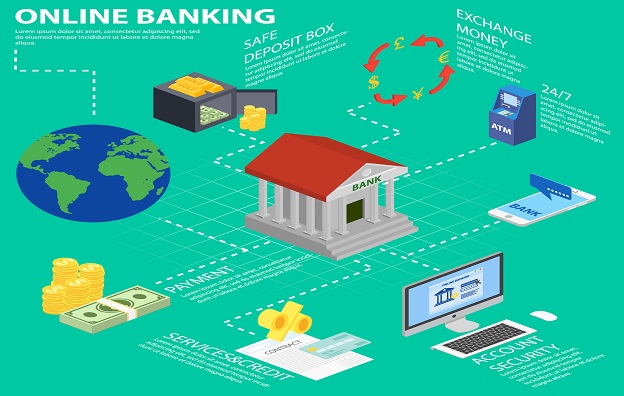

How to help your customers eliminate the ‘Go to the Bank’ from their to-do list

When most people think about the term “Bank” they probably envision a retail branch with long queues, behind a rope waiting to seek the services of a teller or branch representative. Well those days are becoming more and more obsolete, as Gen Y and Millennials are seeking convenient, innovative, digital means of banking. Banks need […]

Your customers have adopted digital payments. Have you?

From being a cash-oriented economy, India has transformed its payment sector to a large extent. The boom in digital payments is attributed to various factors like smartphone penetration and progressive regulatory policies. Especially after the Government of India passed the Demonetization Act in 2016, both the urban and rural population have adopted digital payment solutions […]

Future Banking – Taking a Peek

The future of banking will be so much more than just banking. It will go beyond digital offerings such as real time payments, checking balances, paying bills and making mobile check deposits. The future banks will be data houses that will utilize a customer’s data to weave a financial and personal information avatar of each […]

Mobile Wallets – The New Way to Transact

Gone are the days when the core purpose of a wallet was to hold your cash and cards apart from stuff like a license or a random bill paper. With the advent of digital wallets, the physical wallet is now boiling down to being mainly a fashion accessory. In case you are still wondering what […]

Digitalization of Payments in The Insurance Sector – What It Means for You

The ripples of technology have touched every other industry or rather human lives on a whole. For those insurers ready to seize the moment, digitalization offers an enormous opportunity. The companies that stand to benefit the most are those who are eager to explore the facets of digital payment to reorganize all their operations, from […]

Innovating for A Fast and Secure Future of Payments

The payments industry has been one of the most active areas of innovation in the banking industry. Fintech Firms and payment solutions company are fast transforming the P2P(person to person) and B2B(business to business) payments sector. Cash & cheques, which were the norms back in the day, are now giving way to contactless and chip-based […]

The Evolving Needs of Merchant Management System

Digital disruption has changed the way businesses are executed these days. With multifarious payment options, there is a need to think and redesign the ways merchants are handled by competitive banks. Being able to accept payments through myriad channels from your customers is one of the most important elements of accelerating your business. Payment regulators […]

Growth of Cashless & Real-time Payments (UPI) in India

Introduction of UPI in 2016 and the succeeding UPI 2.0 in 2018, turned out to be a game-changer for the payment landscape in India, taking the country a step closer to a cashless economy. An end-to-end digital transacting platform, UPI has revolutionized the payment structure by bringing multiple banking features, seamless fund routing & merchant […]

Rationalizing Payment & Collections Using POBO COBO Models

Transaction banking refers to the movement of money from one place to another. It is the area of banking that addresses the operational needs and day-to-day transactions of business, corporate and institutional customers. Thus, payments and collections form an integral part of transactional banking. In today’s modern world, all major corporations have their business operations […]